Securities as an economic category and legislative treatment of them Part I.

Part IV.

"Entities are not simply material objects, but material objects

whose source of value is their natural useful properties. The

source of value of documents1(including securities) is information,

that is, social rather than natural qualities." The origin of securities as a particular object of property turnover is

linked to the historical period when people needing to transfer large

quantities of goods and money were faced with a lack of economically

justified means to make such a transfer.

Lawyers found a solution as long ago as 6–5 B.C., when they had the sense to convert the very documents that certified concrete transactions into a special kind of commodity, a special value system, that coincided neither with goods in the proper sense of the word nor with money. Until transaction documents were completed in the form of clay or wax tablets, or on papyrus or parchment, they were not widely in circulation. Paper was invented in the 6th century in China, and in the 9th and 10th centuries, its method of production became known in Western Europe. It was then, under conditions of a natural economy and feudal division, a long way away from a market economy, that paper documents concerning concrete transactions received general recognition and distribution as a particular object of economic circulation.

Securities are shares, bonds, promissory notes and other (including

derivative) certificates of property rights (rights to resources), which

have been separated from their basis and are recognised in this capacity

by legislation.

The federal law dated 29 April 1996 No. 39-FL «On the securities market» specifies that «…a security…is characterised… by the following indicators: it secures the aggregate of property and non-property rights subject to certification, concession and unconditional execution in accordance with the forms and order established by this federal law». There is also a definition of a security in Article 142 of the CC RF: «A security is a document34 that certifies…property rights…». However, it follows from this that there is a mistake in Article 128 of the CC RF, which places securities among goods, as a document which reflects a law of obligation vested in it is an obligation, but not an object. In paragraph 2 of Article 147 of the CC RF, the contractual nature of securities is directly referred to: «Refusal to fulfil an obligation certified by a security, with reference to the obligation’s lack of foundation or its invalidity, is prohibited». We understand goods to mean material objects of the external world. They include both objects of material and spiritual culture, that is, products of human labour, and objects created by nature itself and used by people in their life’s work — land, useful minerals, plants, and so on. The most important characteristic of goods, due to which they are also becoming objects of civil law, is their capacity to satisfy all sorts of human needs. Each type of legal relations with different types of property, as a rule, corresponds to its own type of security, which in turn can play a part in civil transactions (Table 2).

There are dozens of types of securities. They are distinguishable by

the rights and obligations, which are vested in them, of the creditor

(purchaser of the security) and the issuer of the securities. However,

not all of them are distinguished when reflected in business accounts

(a few types of securities that have similar features can be singled

out).

Bond — this is a security that certifies the right of the holder to receive

from the party that issued the obligation, within the specified

period, the nominal value of the bond or some material equivalent.

A bond also grants its holder the right to receive the interest stated in it

on the nominal value of the bond or other proprietary interest (Article

816 of the CC RF). A bond can provide for other proprietary interest

of the holder, if this does not contradict the legislation of the Russian

Federation. Bonds can be issued by the State, and by private companies

in order to raise loan capital (Article 2 of Federal Law No. 39-FL on

the securities market, dated 22 April 1996). Bonds provided by a mortgage

give their holders an additional guarantee against loss of their

funds, as a mortgage gives the owner of the bonds the right to sell mortgaged

property in the event that a company is not in the position to

realise due payments. However, unsecured bonds also exist, which are

debt securities based only on trust in the credit rating of a company, but not guaranteed by any property. Such bonds are issued by companies

in a stable financial position.

Bill/Promissory note — this document certifies the in no way stipulated

obligation of the drawer of the bill (promissory note) or of any

other payer mentioned in the bill (bill of exchange) to pay borrowed

monies at maturity of the bill (Article 815 of the CC RF).

Cheque — this is a security containing an unspecified order of the

issuer to the bank to effect payment to the holder of the cheque of the

amount specified in the order. Only the bank where the issuer holds

funds, which he is entitled to manage by issuing cheques, can be listed

as the cheque payer (Article 877 of the CC RF).

Savings (deposit) certificate — this security certifies the sum of an

investment in a bank and the right of the investor (certificate holder)

to receive the sum of the investment upon the expiry of a set date as well

as the interest, stipulated in the certificate, at the bank which issued the

certificate, or at any subsidiary of this bank. Savings (deposit) certificates

may be bearer certificates or nominal certificates. In the event of

premature presentation of a savings (deposit) certificate for payment

by the bank, the sum of the investment and interest are paid for call

deposits, if a different rate of interest has not been set by the conditions

of the certificate (Article 844 of the CC RF).

Share — this is an equity security which secures the rights of its

owner (shareholder) to receive part of the profits of a joint-stock company

in the form of dividends, to participate in the management of the

company, and to own part of the stock remaining after its liquidation

(Article 2 of the Federal Law «On the securities market»).

A whole range of secondary securities (derivatives) also exists, which

secure the rights and obligations of the issuer and the investor in relation

to the fulfilment of certain operations with securities. This kind of securities

includes options, futures and indices.

Option — this is a short-term security, which grants its owner the

right to buy or sell another security during a specified period for a fixed

price to a contracting party which, for a price, takes on the obligation

to realise this right.

Financial futures — these are standard short-term contracts for the

purchase or sale of a certain security for a fixed price on a fixed date in the future. If the owner of an option may waive his right, having lost

the cash bonus which he paid to the contracting agent, then the futures

contract is compulsory for the subsequent performance.

Negotiability — this is the capacity of a security to independently participate in civil-legal transactions through simplified procedure, for example, by performing an endorsement or simple transfer of a bearer security (Article 146 of the CC RF). Negotiability indicates that a security exists as a special commodity which, consequently, must have its own market with organisation distinctive to it, codes of practice, and so on. Most of those resources, whose owners’ rights are reflected by securities, must also belong to the market as goods. Availability for civil transactions means that a security must represent title of ownership: for example, commodity circulation of weapons, pharmaceuticals, and so on is restricted. Commonality means that a security must have clearly standardised properties that are defined by law (face value, place of issue, etc.). It is precisely this which simplifies the circulation of goods and gives it State protection.

"Bearer securities (Inhaberpapiere, les titres au porteur) comprise one type of securities. Therefore an account of the study of bearer securities would be a useful preface to some preliminary words on the legal nature of securities in general. The very term «securities» (Werthpapiere, les valeurs or les effets) until now has not had a precise definition, either in spoken language or in legislation. Additional terms are needed to describe the concept of securities, such as interest-bearing, credit, monetary and commodity securities. But none of these are notable for their accuracy. Not every security bears a particular interest, like, for example, a bill of lading, invoice, warrant certificate, tickets for travel by rail and sea, theatre and concert tickets, and so on. In other words, not every security is interest-bearing. Furthermore, not all securities are based exclusively on an obligation, i.e. they do not all grant the legal owner the right of demand from a particular debtor; as do shares, for example. Consequently, the term «credit securities» does not embrace all types of securities. There is a multitude of securities of which the subject is not a specific

sum of money, but rather some kind of entity — such as all the

traditional securities: bill of lading, invoice, warrant certificate; therefore,

the term «monetary securities is not a well-founded one. Finally,

not every security is at the same time the object of trade transactions,

such as, for example, dinner and theatre passes, etc.; thus the term

«commodity securities» also proves to be inaccurate.

In legal literature the term «securities» is fairly widely used, especially

from the second half of this (19th — note by the Editor) century

onwards. But there is much disagreement among lawyers on the question

of the concept of these securities. Some confine the concept of

securities to order securities and nameless securities; others include

registered securities (Rectapapiere), such as, for example, nominal

shares. Some exclude passenger tickets, dinner passes, entrance tickets

to public shows, etc., from the concept of securities. Hahn, a commentator

on the German Civil Code, even includes paper money and

postage stamps in the category of securities. Famous commercialist

Thol considers securities to be any documents with proprietary-legal

content, so in this he includes a freight letter, a broker’s note and a

loan obligation. Endemann regards securities as representatives of

value (Werthtrager). According to him, the security itself has no real

value, like any other physical object, but is a bearer of value. The

value is based on trust that the debtor (the issuer of the document)

will fulfil his promise. Therefore, the value of similar document is

based on credit. Endemann counts as securities, among others, State

paper currency, which is also a representative of value, as it embodies the opportunity to be realised (exchanged for metal coins) in the future.

The most widespread definition is that securities are an obligation

embodied in a document (verkorperte Forderungsrechte).

Brunner opposes this definition. He says that rights cannot have a

body in which they are personified. Following this theory, one has to

distinguish between corporeal and incorporeal rights (korperliche und

unkorperliche Rechte). But Brunner’s observation is more witty than essentially

correct. In saying that an obligation is embodied in a document,

lawyers aim to point out the close link between the law and the document,

and the considerable significance of this for the law that results from it,

an idea which Brunner himself expresses in his final pages.

Knies’ definition differs in its comparatively high precision. Having

analysed the distinguishing features of securities, he arrives, finally, at

the following descriptive definition: a security exists when a right is so

closely linked with a document that its owner may demand realisation

from the counter party. Just as ownership of an object is transferred

through the extradition of said object, so the right of demand to a

specified sum of money or a certain commodity in another’s possession

changes through the transfer of a security whose contents consists of

the cited sum of money or commodity.

There is a similar discrepancy in opinions due to the lack of a precise

definition of the legal nature of securities. The majority of lawyers either

do not dwell on this question at all, or give an imprecise definition.

Instead of giving a definition of securities in several words, we shall

point out their essential characteristics.

Securities become such as a result of the right that lies in the document.

The document itself has no value (not taking into account the

material, of course); the value only comes from the right which the

document expresses. Therefore, the essence of securities is that connection

that exists between said right and the document.

Therefore, the first essential feature in the concept of securities is

that they are documents about individual rights41. A document concerning civil law can have threefold significance: the establishment, transfer

or realisation of a right. A document by means of which a right is

established may, in turn, have double significance: either it serves as a

simple means of proof, a surface form of the legal act, or it has considerable

significance for the origin of this right (corpus negotii), as

without the document there is no right. It is essential for the concept

of securities that a right is closely linked with the document, and that

ownership of the document is considered a necessary condition for

the accomplishment of the aim for which the document serves. It

follows from this that a document, as simple proof of the establishment

of such legal relations, cannot be regarded as a security, if only

realisation or transfer of the right are not granted through ownership

of the document.

Thus it is essential for the concept of a security that a document has

considerable significance either for the origin, or the transfer, or the

realisation of the right.

Securities arise principally in the interests of facilitating the transferability

or realisation of a right, but attention can also be drawn to a type

of security in which the aspect of circulatability is lacking: for example,

nominal shares, the transfer of which is normally carried out according

to the principles of cessio. Nevertheless, they are securities, because

ownership of the document is considered an essential aspect in the

matter of using the right associated with that share. This can also be

said of other types of registered documents of commodity circulation

(Rectapapiere).

The abovementioned essential aspect of the concept of securities

(with the ownership of a document, the realisation of its rights are

begun) determines the following logical consequences.

1. The property of the creditor in relation to securities is based on

the moment of formal legitimisation, that is, the creditor is considered

to be whoever has ownership of the document, and ownership, in turn,

is governed by legitimate possession of the document. Legitimate possession

here is the irrefutable assumption of the rights of ownership

(praesumptio juris et de jure). The debtor, fulfilling his obligations in the

name of the owner, is freed from further responsibility, although it

subsequently proved that the document passed to the owner not from

the proprietor. The latter has only a personal action against the direct infringer of his rights. For example, a depository sold bearer securities

that were in his custody or got reparation for them from the debtor. In

the first case, the rights of ownership to the document and the rights

linked to it are transferred to the bona fide purchaser, and in the second

case, the debtor is definitively freed from further responsibility. The

depositor, whose interests were infringed by similar actions of the depository,

may seek damages only from the latter as a direct infringer of

his rights.

2. Securities cannot be liable to vindication in accordance with the

principles of civil law. The very use of vindications for securities has a

different meaning, as the objective of such a replevin is not the return

of the document as such, but the recovery of the rights closely linked

with it. Moreover, the rigorism of this regulation is relaxed by special

decree of positive legislation.

3. In the event that a document is lost or destroyed, the right connected

with it must also discontinue. Positive legislation makes it possible

in such cases to recreate the previous status through amortisation

or cancellation of the lost document and payments in exchange for a

duplicate.

4. Document ownership is also considered a necessary condition for

transfer of the right to it, regardless of whether it is a matter of transferring

rights of ownership or of establishing a mortgage right»42

Securities as unilateral contracts In essence a security is none other than a unilateral contract43 concluded

in a single copy, in which one of the parties may be changed without

the agreement of the other party (freely traded obligation). «Let us

note that negotiability is a very important legal characteristic. The difference

between a traded security (bond, promissory note) and a simple

debt payment lies in the lack of formalities such as notification of the

debtor. The purchaser conscientiously, for a price, acquires the legal title of holder of the traded security, which is free of any defects. By

contrast, a simple assignor of a debt acquires only such a title as was

actually held by the assignee, and is subject to any actions of third parties.

Thus circulatability ensures «pure» relations between each subsequent

holder of the security and the issuer»44.

In support of this theoretical premise of circulatability, the CC RF

claims that rights cannot be certified by a security that is inextricably

linked with the identity of the creditor, particularly claims for alimony

and reimbursement of damages caused to life and health.

Jhering states that a bearer security is only legally a secure means of

establishing (Begrundung) an obligation45.

Nersesov quotes the theory of a unilateral promise as the source of

bearer securities: «Securities arise due to the one-sided actions of a

debtor, who prepares a document, signs it and in so doing creates a new

value. The conditions of validity of the document must be served exclusively

on behalf of the debtor. However, the document, while it remains

in the hands of the debtor, does not have value, it is only a piece

of paper, and only acquires value upon transfer into the hands of another.

The wishes of the latter (the acquirer) are circumstantial and play

a subsidiary role or, rather, this second aspect is a condition (conditio)

under which said security acquires legal validity. Thus the document as

such is considered valid due to the will of the debtor unilaterally represented

in it, but its practical effect is frozen until it passes into the

hands of the acquirer»46

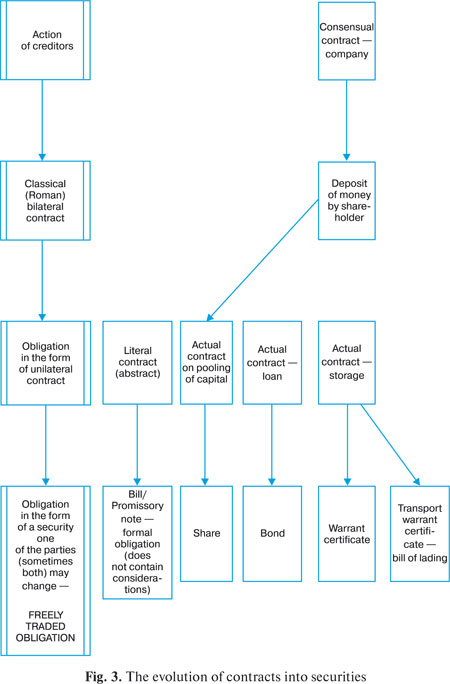

The evolution of contracts into securities Particular attention should be paid to the fact that such contracts

are unilateral only and in them the issuer always gives the obligation,

while the holder is always the «creditor». It is important to note that

real contracts of this type can instantly be drawn up in the form of a

security, whereas consensual contracts are presented in such a form as a result of the fulfilment by the «creditor»-holder of his (usually first)

obligation.

From our reasoning we arrive at the diagram shown in Fig. 3, from

which it follows that:

Section IV of the CC RF, «Individual types of obligations», corroborates this, stating that securities certify property rights resulting from contracts including loan agreements (Articles 815–817), bank deposit agreements (Article 844), cheque payment contracts (Article 877) and warehouse storage agreements (Article 912). It should be noted that rights certified by a security are never corporeal,

but are always of a contractual nature, as they define legal relations

between two parties.

"A transfer note, assignatio and other such legal relations also recognised

by our legislation demonstrate the possibility of acquisition by an outside party of the right of demand from a contract concluded by

others"48

The emergence of securities simplified the certification of ownership

of rights to a defined entity (legitimisation). Legitimisation using a

security must be accomplished exclusively by formal methods, which

obliges one not to take into account any other circumstances, even

those that discredit the owner of a document (therein lies the feature

of public reliability of a security). In relation to a security, the debtor

does not have the right to verify whether the party demanding fulfilment

is his creditor. In order to free himself from responsibility associated

with the security, the debtor must fulfil the requirement of the party

that is responsible according to the officially established formal indicators.

So, powers in relation to a bearer security belonged to its actual

owner, while powers for registered and order securities belonged to the

owner of the corresponding document with an indication of the owner

as the first acquirer or endorsee (originally registered securities, as a

rule, could be transferred using endorsements on general foundations

with order securities). Therefore to transfer rights it was necessary only

to complete the procedure required and sufficient for future legitimisation

of the acquirer of rights before the debtor for a security. Such a

transfer could take place by means of a simple delivery of the document

(security with or without an endorsement) to the acquirer of rights.

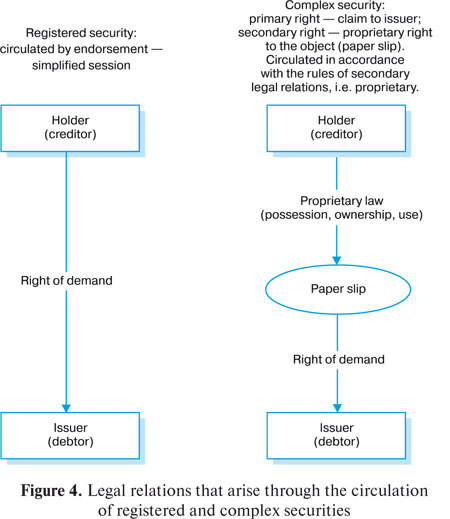

Bearer securities as complex legal relations In any registered (order) security, the holder is defined by an indication

of an individual sign of the party — name or title (sometimes address).

Only in a bearer security the bearer’s right of ownership signifies

the right to make demands to the issuer — and this is an exceptional case.

The second paragraph of Article 142 of the CC RF is only applied in

this exceptional case: «With the transfer of a security, all of its rights are

transferred in aggregate», because in an unethical transfer of a registered

security, rights of claim towards the issuer remain with the previous

holder of the security.

But even in this exceptional case, there is an argument for recognising

a bearer security as an obligation. The fact is that the very word for

bill/promissory note in Russian — вексель (vieksiel) — arrived in the

Russian language from German, in which it is pronounced very similarly

— Wechsel. The primary meaning of the word Wechsel is exchange.

In this case it is translated as «exchange document», «that which can

be changed». And, of course, in English it is translated as promissory

note. Thus, in the English language, the very concept of the promissory

note is formed from the nature of an object, and a ready-made

foreign (German) name arrived in Russia, which did not disclose its

nature.

By analysing this problem a little more thoroughly, we see that a

bearer security is a derivative security, the simplest derivative.

Unfortunately, the existence of complex securities is not mentioned

in the CC RF, and neither do securities as futures, forwards, converted

contracts for the supply of exchange goods, index securities and more

complex futures for index securities feature in Russia’s legal sphere.

Let us compare the legal relations shown in Figure 4.

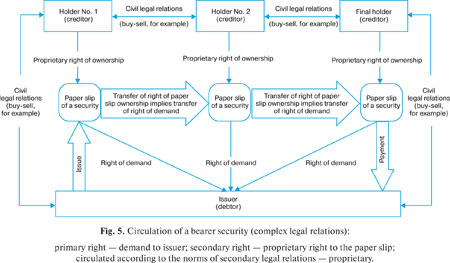

"From our definition of unnamed documents, it is clear that the bearer form is the last step in the historical process of facilitating methods of transfer of obligations. A lot of time had to pass between the unconditional non-transferability of obligations, which was the case for all peoples at the first level of legal development, and equating them with real objects through bearer forms"49

"If we examine unnamed documents at the crucial moments of their

existence, i.e. at the beginning (when they come into being) and at the

end (when they are satisfied), then they become obligatory relations

(obligatio); and if we examine them in their period of existence in material

turnover (in circulation, negotiations), then they become real

objects, like each res"50

We can note here that when such an «unnamed» security is in circulation,

people make use of the rules that are applied to objects, but

the nature of these securities nevertheless remains obligatory.

"When it is necessary to deal with bearer securities while they are

being circulated in civil turnover, the standards of proprietary law must

be applied to them. Unnamed documents can be the object of possession,

ownership, mortgaging and so on. The right of ownership to them

is acquired in the same way as the right of ownership to personal property

is acquired. Possession here is assumed at conscientious ownership;

this assumption is irrefutable (praesumptio juris et de jure). To put it

simply, for bearer securities, as for securities in general, one must make

a distinction between the right to a document and the right from a document.

The first is provided for by conscientious acquisition of the document,

the second, by simple, factual ownership; the first is dealt with

in accordance with the rules of proprietary law, and the second in accordance

with the rules of law of obligations.

The legal basis of the origin of bearer securities is the unilateral

promise of the debtor; in order to acquire the rights from these it is

necessary to own the document.

Bearer securities are unilateral formal obligations in circulation, like

real entities»51 (Fig. 5).

"Some institutions of civil law are, so to speak, caught between proprietary

law and law of obligations. This also relates to bearer securities.

By some characteristics they are subject to the definitions of law of

obligations, and by others, to proprietary law"52

Let it be repeated once again that the above relates to bearer securities

only, and in no way applies to registered securities.

Inadequacy of economic nature and modern legislative treatment of securities "It would not be wrong for us to attribute the main reason for the difference of opinion in the legal nature of unnamed securities to the influence of the prevailing dogma of Roman law. According to the theory of the latter, there is a pronounced difference between the areas of proprietary and contractual law; res and obligatio are two legal concepts that stand in marked contrast to each other. Counting bearer securities as obligations, German legal experts saw, at the same time, that it was impossible to apply to them all the conclusions of Roman contractual law. Meanwhile, in the law of modern peoples, this marked difference between these areas of civil law does not exist"53 The first error in the existing CC RF is the absence of any differentiation

between the following laws:

- obligation — the right of demand, expressed in a security; - proprietary interest in the material bearer of the right of demand. In the overwhelming majority of cases, the value of the material

bearer of demand (material object) is incommensurably less than the

value of the right of demand (obligation) conveyed in this object. The

value of the object can therefore be disregarded, applying the mathematical

concept of «little-o». Thus, it is necessary to imply the right of demand under the term «security» — a freely traded obligation, expressed

through some kind of material bearer (usually paper).

In the legal sense, securities are documents which are valuable, not a

material object on the strength of their natural properties, but due to the

right to some value that is contained in them..

As D. V. Murzin correctly emphasises, «a security represents value

not in itself, even being a material object, but acts as an instrument for

the definition of the essence and magnitude of transferred rights»54

The second error in the CC RF is the expansion of specific proprietary

rules for the treatment of bearer securities to all other securities.

Murzin, having analysed the features of securities, arrived at the conclusion

that «the concept of the security in part 1, paragraph 1, Article

142 of the CC RF relates, most likely, only to bearer securities, and the

exceptions are so prevalent that they make the dogmatic definition itself

an exception to the general rule»55

According to G. F. Shershenevich, registered securities cannot be

called entities56, while R. Savatier has suggested that only a record in

the appropriate books transfers a right that is represented in a registered

security.57

In fact, registered securities are not handled in accordance with the

principle of «the right to a document», because the right is precisely

consolidated between two clearly defined parties.

The right to a document and the right from a document The need to make property relations more dynamic led to the appearance

of legal constructions which made it possible to include rights

in property turnover like real objects. The expression «the right is embodied

in the document», or something similar, is usually used to describe

this phenomenon. However, M. M. Agarkov believes that «this formula should not be given greater significance than a figurative expression

which does not have the level of precision that is necessary in

legal constructions".58

L. Enneccerus elaborated thus: «In securities, the right to the paper,

as to a document, follows from the right that is expressed in the paper,

whereas for bearer securities and order securities, the right coming from

the paper comes from the right to the paper, as to a document".59

K.I. Sklovsky, describing the historical priority of property rights

over contractual rights, remarks: «Contractual rights are used in known

cases as a fiction of an entity, forming incorporeal entities and, on this

basis, the ‘right to a right’"60

With regard to the expressions «right to the document» and «right

from the document», it ought to be noted that the phrases «right to the

medium» and «right from the medium» seem to be more correct when

the media can be:

But computer records, such as:

It follows from this that, for the party that is not effecting the fixation

of property rights in the transaction, this right has no proprietary,

material expression.

When depositing securities in a bank custody account, their transition

from tangible — material (on a paper medium) — into intangible — immaterial

(non-cash — in the form of deeds to a custody account) — does

not change the essence of the securities, their nature and their value

content. Only the medium on which they are represented changes.

Property rights reflected in an obligation are not changed when the

medium of the obligations changes.

At the same time, the principle of the «right from a document» is

completely inapplicable to registered causal securities, as it makes

absolutely no difference who has this security or whether it exists at all,

because the commanding role in this instance is acquired by the entry

made in the register of the party that is obliged in these legal relations,

not by the record on the security.

Neither will this principle ever be applicable to non-cash, uncertificated

securities, because these do not have a medium expressed for

the right holder. And it is in precisely these securities that the principle

of the supremacy of the register becomes exclusive.

Moreover, using the logical method of argument a contrario, one

can logically conclude that, if the proprietary right of ownership to

one’s own paper copy of a contract, such as a loan, exists, then the loan

is a property right, which is incorrect. (If B comes from A, and B is

false, than A is false.)

Thus, using a number of methods, we have explained that a security

is not an object, but a type of contract (agreement)..

To any critics of this point of view I pose the question: what is the pivotal difference between a loan agreement (contract) and an obligation, which makes it possible to ascribe a loan agreement to the sphere of law of obligations, and an obligation to the sphere of property law? The answer is that there is no pivotal difference, as is confirmed by

Article 816 of the CC RF: «In cases provided for by law or other legal

acts, a loan agreement may be concluded by issuing or selling obligations»

(author’s bold).

|

Copying information from this website is only allowed under condition of referring to this web link.

Copyright © 2008 Andrey Gribov

All rights reserved

Russian version

Russian version

{kind=link}