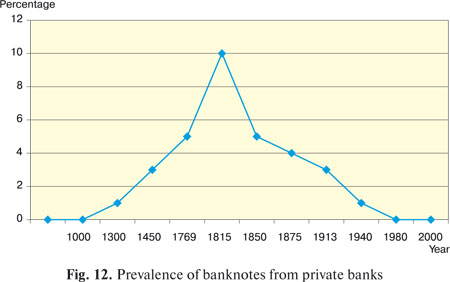

Banknotes from private banks Part I. Part III.

Part IV.

Such liabilities proved more reliable and became very popular, attracting

the maximum demand on the market, giving their bearers an

air of respectability. The Count of Monte-Cristo in Alexandre Dumas’ novel of the

same name boasted that he’s carrying around a one-million bill

from the Rothschilds, and thus greatly impressed his contemporaries. Such bank notes — literally, «notes written by banks», used to be a

proper noun, but became a common noun as time went by.

«A banknote (bank bill) — is a security unified by sum (author’s comment), which certifies the self-addressed order of the issuing bank to pay its bearer immediately upon presentation the sum of money in coins which currently are in circulation119 "A banknote is nothing else but a banker’s bill, according to which

the holder can receive money at any given time and which the banker

uses instead of promissory notes".120" Even though banknotes had the same «bill nature», they were more

stimulating to circulation because of the following properties:

Banknotes, i.e. paper money, don’t have any intrinsic commodity

value. Paper money is a symbol, a sign of exchange value. What then

caused the permanent disappearance of gold from circulation? There

must be objective causes, apart from wars and other troubles, apart from

lavish rulers and cunning bankers. Here is the simplest explanation —

paper money is convenient in circulation, it’s easy to carry. A phrase by

the great Adam Smith comes straight to the point — he said that paper

money must be viewed as a cheaper circulation tool. Consumer value of money impeded circulation, and thus to the front

came exchange value, which caused a process later known as demonetization

— the withdrawing of gold, which no longer performed the

functions of money, from circulation. Circulation Consumer value of nearly all cash credit money consisted in the

quality of the paper and the engraving, which was important to those

with artistic taste, but was worth only about 1 percent of its face value,

which embodied the exchange value of the security in case the issuing

party’s business went well and the beneficiary was aware of that. If,

however, the beneficiary received true or false information that the issuing

party’s business was experiencing difficulties, the security’s exchange

value would begin to decrease. Lastly, if the beneficiary believed

the issuing party to be bankrupt, the security’s exchange value became

equal to its commodity value and depended only upon the beneficiary’s

artistic taste and his wish to keep this particular product of the printing

industry. A banknote from a private bank is a unified by sum «self-addressed»

private bank bearer bill with a non-fixed «upon presentation» term and

a blank endorsement. This derivative security, whilst being an unconditional obligation,

similar to commercial bearer bills, during its issue and paying off was

subject to the law of obligations, within which it is important to specifically

underline the abstract nature of an obligation, caused by the

need to simplify court disputes for the benefit of trade turnover. The essence of the obligation relations which were in place during the paying

off of a banknote, was the unconditional obligation to hand out a

certain amount of precious metal or coins of a certain weight, composition

and form. However, circulation of such banknotes was subject to the more

developed and better known at that time law of estate. The person who

in the physical sense possessed the bill, undoubtedly became the creditor

in this obligation case. The bearer of a banknote had the property right to the banknote

paper bill with an inscription, as well as the unconditional abstract right

to demand precious metals or precious metal coins from the banker. Banknotes were backed by the enormous — by the standards of that

time — wealth of bankers. The wealth of the Rothschilds had been

legendary for a long time. It is necessary to mention that the private law nature of private

banks’ banknotes as a variety of bills provides their holders only with

support in court, in contrast with state-endorsed private law support

provided to holders of currency. |

Copying information from this website is only allowed under condition of referring to this web link.

Copyright © 2008 Andrey Gribov

All rights reserved

Russian version

Russian version