Commercial bills Part I. Part III.

Part IV.

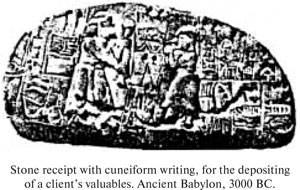

The experience of the Babylonians was then imitated in Ancient

Greece.» 113 Another interesting example is the Tabularium, the most ancient

and secure building in Ancient Rome. Even today, it is partially preserved at the base of the Capitoline hill. There lay clay tablets (tabulas)

on which certified statements for citizens’ tax debts were preserved.

Because there is written evidence that in Ancient Rome one could be

put into slavery for not paying one’s taxes within a set period, it is clear

that these tabulas could be sold by the State to slave owners. There is

more than one case described in which the ‘mob’ revolted, usually ending

up pillaging the Tabularium and breaking the tabulas in half.. The ancient Chinese have been credited with inventing paper money.

In the 10th century China merchants stopped using the heavy iron

coins issued by the Chinese government for small purchases, and used

receipts instead. Receipts started to be used not only for depositing

coins but also for goods, for paying taxes and to issue credit. The use of

these lowered the cost of currency distribution and considerably broadened

trading opportunities. The development of trade relations and wholesale trading was hampered

by coinage being used for major trade. When wholesale trading

developed into deals with silk convoys and ships carrying spice, sacks

and chests full of gold coins were already being used. These were not

very convenient, first of all, because of their large volume, and secondly,

because of the need for reliable storage during shipping. At a time

where there were whole tribes89 of robbers making a living from attacking

trade routes, things became extremely dangerous. In addition to their light weight, commercial bills of sale had one

other advantage: they kept the merchant from being robbed (payment

for bills of sale could only be issued to the actual person named on the

endorsement). Another important quality of the bill of sale was the cheapness and

simplicity of its production — it was not necessary to buy the expensive

metal kept at the mint and the assay office, it was enough just to write

out the paper and endorse it. These bills of sale were civil documents and represented the abstract

obligation of the merchant or trader to pay the person indicated within

a specified period the amount of the specified precious metals. Promissory notes gave rise to a new form of currency: credit. The

producer selling goods on credit received a bill of exchange (a promissory

note) and could use it instead of money to pay for goods purchased

from a third party. The rise of this type of currency as a social phenomenon only came

about because capitalism established close ties between those involved

in public production, much closer than those between traders"114 "The main types of credit currency were bills of exchange, called

«trading» currency by Marx, especially transfer notes, although these

could seldom be used as payment as they could not be endorsed. When

this became legal (around the 17th century), they became more widely

used as payment. In other words, promissory notes used as bills of exchange

became recognised as methods of payment when it started being

used as such. However, commercial bills of sale had several limitations

on their use in domestic exchange, relating to the territory, the times,

those who took part in the exchange, the nominal value (denomination)

of the paper, and warranties. As a result, they could not be universally

accepted. However, if we look at a range of international payments, a

significant number of these were accomplished with bills of exchange:

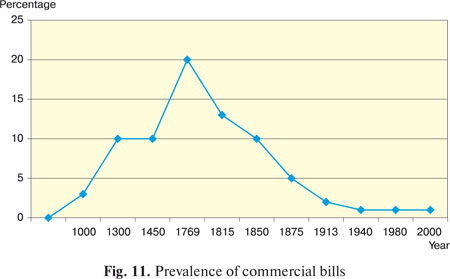

at the turn of the 20th century, these accounted for 80% of all payments.

The fact that they were performing the function of world money is

evident."115. The bill of exchange could be issued by anyone for any sum, any

amount of coins or any weight of gold. These two characteristics — the unlimited number of issuers and the

unrestricted amount of the bill of exchange — significantly limited the

acceptance of the bills, because hardly any beneficiary had reliable

information about the solvency of the issuer and the amounts of the

deals hardly ever matched the amounts the bills were made out to. Gradually, the number of authorised issuers decreased and only

banking establishments that dealt with promissory notes, receiving and

supplying currency as part of their work were recognised, thus getting

rid of the problem of unreliable issuers about whom nothing was

known. Circulation Certified bills of exchange, as already noted, came into being for

convenient circulation in major wholesale trade, and to improve and

make more reliable the deposition of valuables, as well as making production

cheaper and simpler. The backing for these bills was the merchant’s

property, either personal property, that given in exchange, or the merchant’s

success in trading, their caution or ability to earn money. However,

improving the reliability of the depositing and keeping of valuables

made circulation more difficult, as the issuers challenged endorsements

which were not made out in the proper way. Every endorsement was challenged

in local courts and it was possible for only the merchant who had

made the endorsement to be present. Promissory regulations were therefore

drawn up so that any endorser could seek damages in case an issuer

refused payment. This action implied, more or less, the following:

«I trusted you and accepted a bill of exchange from you for this merchant.

But this merchant doesn’t believe me and won’t pay. Take your bill of

exchange and work it out with the merchant». The circulation regulations

deterred traders when there was no reliable or quick long-distance communication.

Only when such communication was made possible did the

promissory notes gain power as a type of money. Merchants — known for their prudence — devised the blank endorsement,

which led to the circulation of blank promissory notes for

bearers and greatly simplified circulation. In this way, anyone bearing

a blank promissory note became a legally bound creditor without question. The bearers’ promissory notes started a new circulation phenomenon:

as derivatives, or derived securities, they allowed the bearer to make concrete transactions and this gave the bearer far more rights in

relation to the issuer. Although the issue and redemption of these promissory

notes complied with the law (abstract requirements for settlement),

the circulation of these notes began to tie in more with the

current development of property rights. The holder of a promissory note to bearer had the right of ownership

on the bill slip with an inscription, and the blank form gave an unconditional

abstract right to request precious metals or coins from the

debtor. The problems with these derived secure documents and their dualist

and legal nature are described in more detail in part 2. It should be noted that the civil nature of the promissory notes only

gives their holder judicial backing as opposed to State support when

used as currency. In the last decade of the 20th century, promissory notes from the

Russian joint stock companies EES Russia, Gazprom and Energoatom

were used to settle existing wholesale accounts, mostly because of the

mistrust of the banking system which had arisen after the two system

level bank crises (in 1995 and 1998). |

Copying information from this website is only allowed under condition of referring to this web link.

Copyright © 2008 Andrey Gribov

All rights reserved

Russian version

Russian version