Stocks and shares, partially fulfilling the functions of money Part I. Part III.

Part IV.

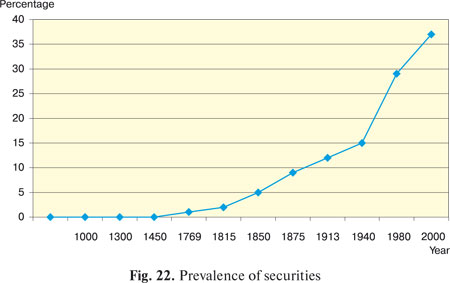

Securities, depending on their type, can, in suitable conditions,

fulfil all the functions of money to some degree (fig. 22):

Let us consider a concrete example: cheques. According to Article 877 of the Civil Code of the Russian Federation

«a cheque is recognised as a security, containing an unconditional instruction by the cheque-giver to the bank, to make a payment of the

sum specified on the cheque to the cheque-bearer.» From the point of view of legislation, transactions made by cheque

are just as common as transactions made by payment order. It is obvious

that cheques fulfil the function of a means of payment and a means of

circulation. Their measure of worth is reflected by the sum inscribed

on the cheque. However, the function of saving/accumulation is essentially

reduced in a cheque, insofar as it is valid for a relatively short

period of time. Although, one must acknowledge that 20–30-year old

banknotes also become invalid in a number of countries. The following example is Minfin bonds, known in Russia as «OGVVZ

» (Obligations of the State Inner Currency Loan). It is obvious that they fulfil the function of a means of payment,

although not in a very wide sector. The main ideologue, which attaches

the payment function to «OGVVZ», was and remains the Russian

Ministry of Finance (Minfin), which offers the possibility to use Minfin

bonds for clearing a debt, buying debts of foreign governments,

carrying out mutual tax-related settlements and regulating/classifying

payments. In transactions between Russian parent companies and their subsidiaries

abroad Minfin bonds are used extremely often as a means of

circulation and even as international currency. Often they are used as a

means of giving credit to subsidiaries abroad. It is necessary to note that,

in contrast to the use of local currency, the use of securities as a means

of payment requires the agreement of the receiver (beneficiary). A means of accumulation easily manifests itself theoretically by the

very nature of a bond as a means of saving, and practically, via the

analysis of fund portfolios of banks, insurance companies and various

funds, which are the most active investors into Minfin bonds. The measure of value is reflected by the document’s face value and

its market rate. Generally speaking, we are concluding that if one or another security

fulfils the function of money, then it is possible to recognize it as

money. In economics, there are many things of which it is impossible to talk

in precise terms. For example, do types of money such as coins actually fulfil the

function of money, in super-wholesale transactions of 1 billion roubles

(33 million US Dollars)176 and over? No, they do not. Does this mean

that coins are not money? Things are not at all simple. It is not possible

to describe one type of money with 100% certainty as ideally fulfilling

the function of money, because:

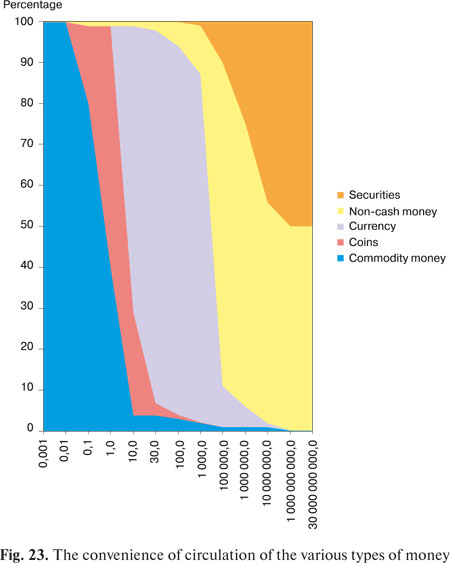

Not one type of money ideally fulfils the function of money; each

type of money is convenient in one or another situation (fig. 23). For example, coins serve the sector of transactions well, when the sum to be paid does not exceed the value of the 10 highest denominations of coins, and, in case of banknotes, when the sum to be paid does not exceed the 300 highest denominations of currency. In relation to bigger deals, cashless methods of payment are more convenient. In a cash-orientated economy, it is not unheard of for expensive property to be bought with cash, but this is moving away from the area of the theory of money, and more a case of the theory of efficient taxation.

|

Copying information from this website is only allowed under condition of referring to this web link.

Copyright © 2008 Andrey Gribov

All rights reserved

Russian version

Russian version