Non-cash currency — deposited money (checking accounts) Part I. Part III.

Part IV.

Deposited money as a form of credit money represents currency in

paperless form. From an economic point of view, the existence and

development are a result of the following: 1. Reducing costs of circulation; 2. Speeding up of circulation; 3. Practicality and comparative security of cashless transactions; 4. Simplicity of supervision of circulation for the State. This form of money has the following important properties:

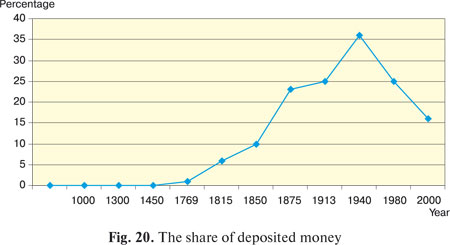

Deposited money acquired the function of money only with the

process of realization of cashless bank accounts i.e. only in the mid 20th

century. This became possible only at the time of a corresponding

level of development of industrial power, in part thanks to the release

of banking mainframes by the company IBM and the introduction of

CHIPS, an electronic system of inter-bank accounts. L.G. Efimova writes: «In connection with this, economists for a long

time did not acknowledge call deposits as being money. When, in 1930,

John Maynard Keynes, in his book «Treatise on Money» included call

deposit in his concept of money, G. Parker Willis, a famous professor

of Colombia University, reacted to this entirely critically162. Amongst

later economists, practically no opponents to this point of view remained163. The problem of the right to issue cashless (credit) money has not

been unequivocally solved by the legislator. Insofar as a ban on cashless

emissions exists, any commercial bank may issue (and does issue) its

money in the form of balances in payment and current accounts. Nobel

Prize laureate Friedrich Hayek spoke out in favour of the issue of private

money167. He proposed that the monetary liability expressed by the currency

issued by any concrete issuer would amount to the nominal value.

However, different types of currency should be freely exchanged according

to the rate of exchange. At the same time F. Hayek spoke out

for the necessity for each issuer to support the value (buying power) of

his currency in relation to the average set of wholesale products (a standard

of price) by means of special, pre-determined measures of influence.

«I expect that, at least in wealthy regions, far exceeding presentday

national territories, people will be willing to regard an average set

of wholesale products as a price standard, in relation to which they

would prefer to safeguard the constancy of their money168. Despite

scepticism from opponents, Hayek’s ideas clearly came to fruition in

Russia, where promissory notes of the company «Gazprom» indeed

fulfil the function of money, in both wholesale transactions and in the

accumulations of financial institutions. The researcher himself suggested

that the full realization of his idea requires corresponding political

reforms, because governments are unlikely to relinquish the profitable privilege of issuing money169. However, his idea about private

money was partly realized in the form of call deposits. Some economists and lawyers suggest that such «private monies» do

not have a cash/tangible form. Here we are forced to disagree and to

point out that «self-addressed» bank bills, issued in exchange for deposits,

which are so widespread now in Russia, are in fact «private

monies». When such money is termed «private», their private-legal

content is implied, in contrast to currency, which has public-legal

content. It is very important to note that their private-legal character applies

only in the relationship between the investor and the private bank,

whilst the legal relationship between the private bank and the State bank

it remains one of a public-legal character. Thus, deposited money (cashless currency), in the form of balances

in the accounts of enterprises and organisations, is money of both

the Central Bank of the Russian Federation and of the commercial

banks. When a customer withdraws money from his account, then, in

essence, one is talking about of the conversion of cashless currency

(deposited money) to cash currency, to the banknotes and coinage of

the Central Bank of the Russian Federation. "Now we will investigate the legal character of non-cash money. For

the purpose of this book, we understand cashless currency as balances

in credit in various client accounts in banks, to which the application of

Chapter 45 of the Civil Code of the Russian Federation extends. They

are accounts which are specially intended for carrying out various

transactions: payment, current, current currency, correspondence, accounts

for the financing of capital investments etc.170 From a legal point

of view, an entry into a bank account serves as a quantitative expression

of the legal-liability claim of the client towards the bank. However, this

circumstance does not impede the recognition of the bank liabilities as

money, taking into account that the latter fulfils the function of a means

of payment. As a liability of the relevant storehouse (bank, depository), cashless

money is subject to the law of obligations. An entry into a bank account attests to what sum (to what measure) the bank is the debtor of its client.

In this way, the legal relationship we are examining appears to be relative

and arises by the will of each party to the bank account contract.

According to this contract, the obligation of the bank consists of the

completion of concrete, positive actions. It should carry out the instructions

of the client in making payments to a third party, in releasing cash

funds to the client within the limits of the balance of his account and

likewise it should accept payments owed to the client. The owner of the

account’s right of demand can be violated above all by the bank, to

which the client has the right to lay the same claim171 At the present time, the overwhelming majority of money in circulation

in Russia is deposited, cashless money, which has almost no

tangible expression (discounting the paper receipts on which bank

statements are printed). In this way, contemporary deposited cashless

money presents itself as a non-document nominal security:

When considering the security of such a form of liabilities, we say

that the liability of the Central Bank itself is secured, just as in the case

of cash currency:

The liability of the private bank should, in theory, be secured by the

aforementioned liabilities of the Central Bank, but in the assets of any

bank, non-cash currency occupies, in accordance with Basle Principles,

no less than 12%, and as a rule, no more than 25%. As a result of the

active credit policy of any bank, its liabilities are fundamentally secured

by the quality of its credit portfolio. Despite unity of form, the means of administration of money, on the

part of the clients, varies from bank to bank, leading to a certain amount

of confusion amongst economists. There is no such thing as «electronic money», but there is an electronic

method of gaining access to deposited funds; there is no «plastic

money», but there is a method of gaining access to accounts with the

help of plastic cards. We will now introduce the basic methods of the administration of

(access to) money:

Circulation This form of money has no consumer value, since it does not exist

in tangible form (perhaps it does possess a certain value of joyful emotion,

arising when the rich man admires his bank balance, but this is

hard to evaluate). The exchange value, as already indicated, depends

only on the generally recognized, current reputation of the issuer, and

also on the short and long-term expectations of fluctuations of the

money in terms of a commodity basket (its buying power). Since the development of a reliable long-distance communications

and computing technology, the banking system was finally able to rid

itself of the complex derivative legal relations. This form of money has

practically no tangible form. It is secured against the right to demand its acceptance in payment

of taxes and for any payment between two legal parties, with the exception

of a relationship known to be retail (not wholesale) commercial.

This exception, of accepting cash currency as payment for goods, is

conditionally licensed by the government in order to support a steady

demand for non-cash currency. Demand for currency Besides generally known factors of demand for money, including

those described by Keynes and Friedman, demand for cash and noncash

currency not guaranteed by gold, forms as a result of the following

factors, which, rather than being of economic character, are of a precisely

juridical, public-legal nature. 1. The necessity of paying taxes. Any upstanding government accepts

only its own currency as payment of taxes. Correspondingly, the

demand for currency depends on:

However, it is sufficiently obvious that high rates of taxation lead to

the flight of industry to other jurisdictions, and low rates of taxation

lead to weakening of the government’s ability to defend its borders and

to maintain order within the sovereign territory. Tax rate in the USA is

the main publicly discussed issue and fluctuates, depending on the

condition of the economy and the general public will, in the region of

20–30%. 2. The necessity of transactions with the State for the purchase of

State property. This is not an overly important factor, which actually

works in the case of the privatisation by the government of wealthy

enterprises. 3. The necessity of having precisely State-supported means of paying

any debt or making any payment within the territory of said State.

This issue arises particularly sharply with the significant risk of disputes

emerging when deals (transactions) are being made. If there is sufficient

faith in the judicial resolution of a conflict, settlement of a debt with

an improper means of payment can be a serious argument against the

payer. But this factor directly depends on the strength of the government.

In periods of discord and change of government, the aforementioned

factor works against the currency or in favour of such privatelegal

liabilities, like bills/promissory notes or bank liabilities or in favour

of natural commodity money. 4. The demand for currency for hoarding purposes, arising as a

result of a lower level of faith in the government, compared to other

issuers. This emerges usually in the case when confidence in one’s own

government or in its ability to keep inflation in check, is essentially

lower than confidence in other governments. An example of this is the

Russians’ total lack of confidence in the Russian rouble as a means of

stabilising prices, arising in part as a result of Pavlov’s reforms, which

withdrew 50 and 100 rouble banknotes from circulation without compensation,

and also as a result of many years of inflation and hyperinflation,

which had regularly cheapened cash and non-cash currency. The

author is personally acquainted with people who had invested

10,000 roubles in Sberbank in the 1980s, which at that time was enough

to buy a «Volga» car or a decent house, and now is enough only to buy

a children’s bike. 5. The demand for currency for hoarding purposes, arising as a

result of confidence in a government which capably supports a reliable

and functional banking system. For example, the total collapse of the

banking system in 1998 does not facilitate long-term storage of money,

in the form of long-term rouble deposits. A series of experts (the author included) believe that the fundamental

causes of bank crises are not so much the sharp fluctuations in

property prices (for building societies), in share prices (for investment

banks), currency etc., as much as the incorrect fulfilment by the government

of its regulatory function, which involves not allowing the warping

of the credit portfolios of banks in one or another branch of the

economy. For example, in the USA after the crisis of 1930–1933 banks

were prohibited by legislation from acquiring shares. 6. Convenient currency legislation. If the government prohibits the

circulation of its own currency abroad, it is difficult for it to hope that

foreign citizens and businesses will accumulate this currency. |

Copying information from this website is only allowed under condition of referring to this web link.

Copyright © 2008 Andrey Gribov

All rights reserved

Russian version

Russian version